How Do Next-Generation Money Markets Respond to Donald Trump's Tariff War?

Chaos Labs Risk Report — Original Source

Overview

Following President Trump's announcement of new tariffs on Chinese imports, financial markets experienced one of the most severe and rapid downturns in recent history. Within just 30 minutes, Bitcoin's price dropped over 12%, falling from $116,500 to $102,700. Ether suffered an even more brutal correction of roughly 20%, while many other assets plummeted by over 50–60% in just 10 minutes.

This abrupt market dislocation triggered massive liquidation cascades across DeFi and CeFi platforms. Notably, thanks to the accumulation of liquidation bonuses that far exceeded the increase in deficit, Aave closed the event with a net profit of $1.5 million, despite $180 million in liquidations.

Liquidation Volume

The market downturn triggered a widespread wave of liquidations across Aave instances, primarily concentrated in the BTC, ETH, and WSTETH markets. The total on-chain liquidation volume reached approximately $180 million.

The event generated approximately $10 million in liquidation bonuses, of which $1 million was returned to the DAO treasury as liquidation fees.

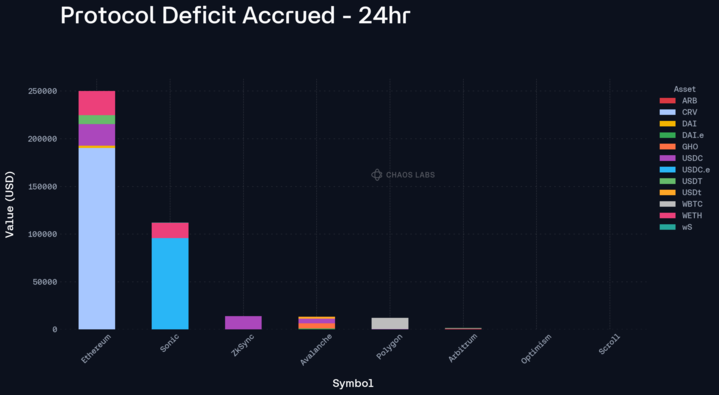

Bad Debt

Due to the market crash, certain positions could not be closed because of insufficient liquidity, gas fee spikes, and significant oracle delays. At the time of the report's writing, the protocol had accumulated approximately $400,000 in outstanding deficit.

The majority of this deficit came from debt positions in CRV and ENS, which lacked on-chain liquidity during the crash. This allowed an entity using the generalized ETH configuration (83% LT) to borrow assets whose oracle prices were not updating fast enough relative to actual market prices, resulting in bad debt.

Notable: An ENS debt position, backed by only $2 of ETH collateral against approximately $88,000 of ENS debt, remains unliquidated as the operation would not be profitable. Consequently, this position does not appear in the aggregated deficit data.

Additionally, collateral losses contributing to the deficit primarily came from LINK, wS, and UNI exposures.

These positions represent a manageable shortfall as market conditions stabilize.

SVR (Smart Value Recapture)

SVR liquidations generated approximately $1 million in additional revenue for the DAO, on a liquidation volume of $35 million, primarily from WETH and BTC flows.

However, the event temporarily revealed oracle weaknesses, with price updates delayed by 5 blocks on certain markets. During this delay, on-chain prices for the AAVE and LINK SVR feeds deviated by 45% and 32% respectively from their theoretical value, while ETH showed a 6.51% dislocation.

In practical terms, this means that during severe price deviations where oracles were attempting to update at nearly every block, the SVR feed delay caused a single abrupt price update after the cutoff window, leading to 30–40% price gaps and the instant appearance of deficits. Since market prices rebounded shortly after, these delays did not cause additional losses. Nevertheless, had the decline persisted, this lag could have worsened the bad debt.

Conclusion

Overall, this flash crash resulted in approximately $500,000 in bad debt and expected deficit, primarily due to the illiquidity of CRV and ENS positions. While this is a moderately negative outcome on these specific points, it was offset by liquidation activity that generated approximately $1 million in liquidation fees and an additional $1 million through SVR liquidations.

The protocol remains net positive overall, with an estimated profit of $1.5 million from this event.